Top 6 accounting mistakes small businesses make

As an accounting firm based in Putney and Richmond, we’ve seen our fair share of small business owners make accounting mistakes.

These mistakes can cost you time, money, and even your business. Fortunately, they are quite easy to avoid and with the assistance of a professional accountant, you’ll never need to be concerned about making them again.

In this article, we’re going to share the top 6 accounting mistakes small businesses make, and how you can avoid them.

Mistake #1: Not Keeping Good Records

This is one of the most common accounting mistakes we see. Small business owners often don’t think it’s important to keep track of their receipts, invoices, and other financial documents. But this is a big mistake!

Good records are essential for tracking your income and expenses, filing your taxes, and getting loans or financing. If you don’t keep good records, you’ll be flying blind when it comes to your finances.

Here are some examples of the importance of keeping good records:

- If you don’t keep track of your income and expenses, you won’t know how much money you’re making or spending. This can lead to overspending and financial problems.

- If you don’t file your taxes on time, you could be subject to penalties and interest.

- If you don’t keep good records, it will be difficult to get a loan or financing. Lenders want to see that you’re a responsible business owner who can manage your finances.

Here are some tips for keeping good records:

- Get a receipt for every purchase you make for your business.

- Keep all of your invoices and other financial documents in a safe place.

- Back up your records regularly.

- Use accounting software, such as Xero, to help you track your income and expenses.

Mistake #2: Not Paying Your Taxes on Time

The penalties for late tax payments can be significant, so it’s important to make sure you pay your taxes on time. If you’re not sure when your taxes are due, you can always check with HMRC.

Here are some tips for paying your taxes on time:

- Set up a system for tracking your tax deadlines.

- Make sure you have enough money to pay your taxes on time.

- File your taxes electronically.

- Get professional accounting help if you need it.

Mistake #3: Not Using Accounting Software

Accounting software can save you a lot of time and hassle. It can help you track your income and expenses, generate reports, and file your taxes. There are many different accounting software programs available, so you can find one that fits your needs and budget. We recommend cloud based accounting from companies like Xero.

Here are some of the benefits of using accounting software:

- Increased accuracy

- Improved efficiency

- Reduced costs

- Easier compliance

Mistake #4: Not Getting Help from a Professional

If you’re not comfortable handling your own accounting, there are many qualified accountants who can help you. An accountant can help you set up a sound accounting system, track your finances, and file your taxes.

The cost of hiring an accountant can be offset by the benefits of having accurate and up-to-date financial records.

Here are some of the benefits of hiring an accountant:

- Peace of mind knowing that your finances are in good hands

- Expert advice on tax planning and other financial matters

- Time savings

Mistake #5: Not Planning for the Future

It’s important to plan for the future of your business, and this includes planning for your taxes. You should consult with an accountant to find out how to minimize your tax liability and make the most of your tax deductions.

By planning for the future, you can help ensure that your small business is financially secure.

Here are some tips for planning for the future:

- Consult with an accountant to find out how to minimize your tax liability.

- Make sure you have a plan for retirement.

- Make sure you have a plan for the sale of your business.

Mistake #6: Not Having a Disaster Recovery Plan

A disaster recovery plan is a document that outlines how your business will continue to operate in the event of a disaster, such as a fire, flood, or cyberattack. Having a disaster recovery plan in place can help you minimize the financial impact of a disaster and get your business back up and running as quickly as possible.

Here are some tips for creating a disaster recovery plan:

- Identify your critical systems and data. What are the systems and data that are essential for your business to operate? Once you know what’s critical, you can start to develop a plan for how to protect it.

- Create a backup plan. This should include a plan for backing up your data and systems, as well as a plan for restoring them in the event of a disaster.

- Test your plan regularly. This will help you identify any potential problems and make sure that your plan is up-to-date.

- Communicate your plan to your employees. Everyone in your business should know what to do in the event of a disaster.

- Keep your plan updated. Your business and its needs will change over time, so it’s important to keep your disaster recovery plan updated as well.

By following these tips, you can help ensure that your business is prepared for any disaster.

Why not talk to TaxAgility and see how we can help you avoid these mistakes

By avoiding these common accounting mistakes, you can help ensure the financial health of your small business. So if you’re a small business owner, be sure to keep these tips in mind.

TaxAgility has been helping small businesses in and around Richmond and Putney for many years.

Contact us today on 020 8108 0090 to learn more about how we can help you.

Tips to help you achieve success in a challenging 2023 business environment

We are already one quarter or the way through 2023. The UK economy continues to face a number of challenges this year. With the outlook unlikely to change much during the year, except possible interest rate changes and adjustments in inflation, businesses will need to be more agile and innovative than ever before in order to remain successful. We thought it might be useful to you, to share are a few tips on how to do just that as you progress through the year.

How Businesses Can Remain Successful in 2023

The economic environment in 2023 is uncertain. The UK economy is expected to grow at a slower pace than in 2022, and there are concerns about the impact of rising inflation and interest rates. Despite the uncertainty, there are a number of steps that businesses can take to remain successful in 2023 and set themselves up for success in 2024.  These include:

These include:

Focusing on cash flow: In a challenging economic environment, it is important to focus on cash flow. This means ensuring that you have enough money coming in to cover your expenses. You may need to take steps to reduce your costs, such as negotiating better deals with suppliers or reducing your workforce.

Investing in innovation: Innovation can help you to stay ahead of the competition and create new opportunities. This could involve developing new products or services, or finding new ways to reach your customers.

Building relationships with customers and suppliers: Strong relationships with customers and suppliers can help you to weather difficult economic times. Make sure that you are communicating regularly with your customers and suppliers, and that you are working together to find solutions to any problems that may arise.

Being prepared to adapt: The economic environment is constantly changing, so it is important to be prepared to adapt. This could involve changing your business model, entering new markets, or developing new products or services.

Focus on cash flow

In a challenging economic environment, it is important to focus on cash flow. This means ensuring that you have enough money coming in to cover your expenses. You may need to take steps to reduce your costs, such as negotiating better deals with suppliers or reducing your workforce.

One way to focus on cash flow is to track your income and expenses closely. This will help you to identify areas where you may be able to cut costs. You can use a spreadsheet or a budgeting app to track your finances.

Another way to focus on cash flow is to set up a budget. A budget can help you to track your spending and make sure that you are not spending more money than you are bringing in. When creating a budget, be sure to include all of your income and expenses, both fixed and variable. You may also want to consider creating a separate budget for your business expenses.

Finally, it is important to pay your bills on time. This will help to avoid late fees and damage to your credit score. Late payments can also damage your relationships with your suppliers and customers. Make sure to set up automatic payments for your bills so that you never miss a payment.

Invest in innovation

Innovation can help you to stay ahead of the competition and create new opportunities. This could involve developing new products or services, or finding new ways to reach your customers.

Invest in innovation, such as leveraging AI. AI can be used to automate tasks, improve decision-making, and personalise the customer experience. For example, AI can be used to automate customer service tasks, such as answering frequently asked questions or processing orders. AI can also be used to analyse data and identify patterns that would be difficult for humans to spot. This information can then be used to make better decisions about things like pricing, marketing, and product development.

Don’t forget to continue your digital enablement journey. Automating processes and leveraging the growing base of digital tools can help transform the efficiency of your business.

Finally, AI can be used to personalise the customer experience by providing customers with the information and products they need when they need them.

Listen to your customer’s thoughts on innovation in their businesses. What are their needs and wants? What are they not getting from other businesses? By listening to your customers, you can identify opportunities to develop new products or services that meet their needs.

Consider partnering with other businesses. This can help you to access new technologies and markets. For example, you could partner with a company that specialises in AI to develop new products or services. You could also partner with a company that operates in a different market to expand your reach.

Another way to invest in innovation is to look for new opportunities. Are there new markets that you could enter? Are there new ways to reach your customers? Be sure to stay up-to-date on industry trends and developments so that you can identify new opportunities.

Create a culture of innovation within your business. This means encouraging employees to be creative and to come up with new ideas. You can do this by providing training on innovation, offering rewards for innovative ideas, and creating a space where employees can share their ideas.

Finally, it is important to be willing to take ‘manageable’ risks. Innovation often involves taking risks. Don’t be afraid to fail. Failure is a part of the learning process and can lead to success.

Build relationships with customers and suppliers

Strong relationships with customers and suppliers can help you to weather difficult economic times. Make sure that you are communicating regularly with your customers and suppliers, and that you are working together to find solutions to any problems that may arise.

One way to build relationships with customers is to communicate regularly. This could involve sending out newsletters, holding regular meetings, or simply being available to answer questions. Regular communication can help to build trust and rapport with your customers.

Another way to build relationships with customers is to be responsive to their needs. If they have a problem, be quick to resolve it. By being responsive to your customers’ needs, you can show them that you value their business and that you are committed to providing them with a good experience.

Finally, it is important to be reliable. Do what you say you will do, when you say you will do it. Reliability is essential for building trust with your customers. If you can’t be relied on to keep your promises, your customers will eventually stop doing business with you.

Be prepared to adapt

The economic environment is constantly changing, so it is important to be prepared to adapt. This could involve changing your business model, entering new markets, or developing new products or services.

One way to be prepared to adapt is to be flexible. Be willing to change your plans as needed. The ability to adapt is essential for surviving in a changing economy. If you are too rigid in your thinking, you will likely be left behind.

Another way to be prepared to adapt is to be open to new ideas. Don’t be afraid to try new things. The best way to find out if something will work is to try it. If it doesn’t work, you can always go back to your original plan.

Finally, it is important to be willing to take risks. Sometimes, you need to take risks in order to grow your business. Look out for trends you can seize upon. If you never take any risks, you will never achieve anything great.

By taking these steps, businesses can increase their chances of remaining successful in 2023 and setting themselves up for success in 2024.

Talk to TaxAgility

The business environment in 2023 is uncertain, but it is also full of opportunity. Businesses that are able to adapt and innovate will be well-positioned for success. AI can be a powerful tool for businesses that are able to use it effectively. Businesses that invest in AI now will be ahead of the curve in the years to come.

The future of business is uncertain, but it is also exciting. Businesses that are able to rise to the challenge will be rewarded. The world is changing rapidly, and businesses that are able to adapt will be the ones that succeed.

We encourage you to embrace the challenge of business in 2023. It is a time of great opportunity, and businesses that are able to seize it will be the ones that succeed.

At TaxAgility, we understand the challenges that businesses face in 2023. We are here to help you navigate the uncertain economic environment and grow your business. We offer a wide range of services, including accounting, tax planning, and business consulting. We can help you with everything from cash flow management to strategic planning.

We are committed to helping our clients succeed. We have a team of experienced and knowledgeable professionals who are dedicated to providing our clients with the best possible service. We are here to help you achieve your business goals.

Contact us today on 020 8108 0090 to learn more about how we can help you grow your business in 2023.

Embracing Digital Enablement: How Accountants Empower Business Clients to Thrive in a Digital Era

The digital landscape is transforming the way businesses operate, requiring them to adopt digital enablement strategies to stay competitive and drive growth. Accountants play a crucial role in guiding their clients through this transition, helping them understand and implement digital tools and technologies.

In this article, we will delve deeper into the various ways accountants support their business clients in embracing digital enablement, providing specific examples and detailed insights.

Assessing the digital readiness of clients

Assessing the digital readiness of clients

Building a solid foundation is key to successful digital enablement. Accountants can provide a comprehensive assessment of their clients’ current digital capabilities, identifying areas for improvement and potential growth opportunities. By understanding the unique needs and challenges of each client, accountants can develop tailored strategies that drive digital success.

Before implementing digital enablement strategies, accountants can, with third parties, help clients gauge their digital readiness through a comprehensive review of their:

- Digital infrastructure: Assessing the client’s hardware, software, and network capabilities to determine if upgrades or replacements are needed.

- Processes and workflows: Identifying inefficiencies and bottlenecks that can be addressed through digital tools or automation.

- Digital skills and knowledge: Evaluating the client’s team’s proficiency in using digital tools and technologies, pinpointing areas where additional training may be required.

- Industry trends and competitor analysis: Comparing the client’s digital maturity to industry benchmarks and competitors to identify gaps and opportunities.

Educating clients on the importance of digital enablement

Change can be daunting, especially when it comes to adopting new technologies. To help clients overcome their hesitations and recognize the value of digital enablement, accountants can provide education, resources, and real-world examples. By illuminating the numerous benefits that come with digital adoption, accountants can inspire their clients to embrace innovation with confidence.

To help clients appreciate the value of digital enablement, accountants can:

- Share success stories: Presenting case studies of businesses that have successfully adopted digital technologies and the benefits they have experienced, such as reduced costs, increased revenue, and improved customer satisfaction.

- Highlight government incentives: Informing clients about government grants or incentives available for adopting digital technologies, such as the UK’s Making Tax Digital initiative.

- Discuss future-proofing: Emphasising the importance of digital enablement as a means to future-proof their business against disruptive technologies and evolving customer expectations.

Recommending and implementing digital tools

The right digital tools can revolutionise a business, streamlining processes and unlocking new opportunities. Accountants, with their in-depth understanding of their clients’ operations, can recommend and implement the most effective tools tailored to each client’s unique needs. From cloud accounting software to e-commerce platforms, accountants can help clients harness the power of digital technologies.

Accountants can recommend specific digital tools tailored to their clients’ needs, including:

Cloud accounting software: Platforms like Xero, QuickBooks, and Sage offer robust features, such as real-time financial data access, invoicing, payroll management, and integration with other business tools.

Automation tools: Solutions like Zapier or Automate.io help clients automate repetitive tasks, such as data entry, email notifications, and report generation.

Data analytics tools: Tools like Microsoft Power BI or Tableau enable clients to analyse financial data, identify trends, and make data-driven decisions.

CRM systems: Platforms like Salesforce or HubSpot help businesses manage customer interactions, track leads, and analyse customer behaviour.

E-commerce platforms: Shopify or WooCommerce simplify the process of setting up and managing an online store, allowing businesses to reach a broader audience.

Providing training and support

Adopting new digital tools is only the beginning; clients must also be proficient in using them. Accountants can offer, with specialist third parties, essential training and support, ensuring clients understand how to leverage their new digital tools to their fullest potential. By providing ongoing assistance, accountants can help clients navigate the learning curve and overcome any challenges that arise during their digital journey.

Accountants can offer training and support to clients in various ways:

- Conduct workshops or webinars: Accountants can organise workshops or webinars to train clients on using digital tools effectively.

- Create custom guides and resources: Developing tailored user guides, video tutorials, or other resources can help clients navigate new tools with ease.

- Offer ongoing support: Providing ongoing support through email, phone, or in-person consultations ensures clients can address any challenges that arise during the transition.

Assisting with cybersecurity and data privacy

As businesses embrace digital technologies, they must also prioritise the security of their digital assets and the privacy of their customers’ data. Accountants can help clients navigate the complex world of cybersecurity and data privacy, offering guidance and recommendations to minimise risk and ensure compliance with relevant regulations. By prioritising security, accountants can help clients protect their valuable information and build trust with their customers.

To help clients safeguard their digital assets, accountants can:

- Recommend secure cloud storage solutions: Platforms like Dropbox, Google Drive, or Microsoft OneDrive offer secure storage with encryption and access controls.

- Implement multi-factor authentication: Encouraging the use of multi-factor authentication adds an extra layer of security to clients’ digital accounts.

- Develop policies for data management: Accountants can help clients create policies for data storage, access control, and retention, ensuring compliance with data protection regulations like GDPR.

- Conduct risk assessments: Regularly assessing clients’ digital environment for potential vulnerabilities and recommending appropriate security measures.

- Educate clients on cybersecurity best practices: Providing clients with guidance on password management, software updates, and safe browsing habits to minimise the risk of cyber threats.

Guiding clients through digital transformation

Digital enablement is an ongoing journey, requiring businesses to continuously adapt and innovate. Accountants can serve as trusted advisors throughout this process, helping clients stay ahead of emerging trends and capitalise on new opportunities. By offering strategic advice and expert guidance, accountants can help their clients thrive in the ever-evolving digital landscape.

Accountants can serve as trusted advisors throughout the digital transformation journey by:

- Staying informed about emerging trends and technologies: Accountants can attend conferences, participate in industry forums, and read relevant publications to stay current with the latest digital advancements.

- Offering strategic advice: Based on their knowledge of industry trends and client needs, accountants can provide tailored advice on digital investments, technology adoption, and process improvements.

- Helping clients adapt to new business models: As digital technologies disrupt traditional business models, accountants can assist clients in adapting to new revenue streams, distribution channels, or customer segments.

- Facilitating collaboration and change management: Accountants can help clients navigate the cultural and organisational changes that come with digital transformation by fostering collaboration, communication, and a growth mindset among the team members.

How TaxAgility can help your firm navigate the digital enablement process

TaxAgility can play a critical role in helping you understand and implement digital enablement strategies. By assessing your digital readiness, educating you on the importance of digital enablement, recommending and implementing tailored digital tools, helping identify training and support, assisting with cybersecurity and data privacy, and guiding you through the overall digital transformation process, we help our clients empower their businesses to thrive in an increasingly digital era.

We’re here to assist and advise as problems and opportunities arise. Call us today to discuss how we can help you, on: 020 8108 0090.

Note: This article is not intended to provide financial advice or guidance, it is for interest only.

AI-Powered Accounting: Boosting Efficiency and Value for Small Business Clients

The fear of Artificial Intelligence (AI) replacing human jobs has been around for a long time, and it’s only getting more intense. But here’s the truth: AI is far from being able to replace human labor anytime soon, if ever. In this article, we’ll explore the impact AI is likely to have on the accounting profession and the potential benefits it will bring to both us as accountants and the service we provide to you, our clients.

Debunking the Myth of AI Replacing Accountants

The rapid development of Artificial Intelligence (AI) has generated widespread discussion and, in some cases, apprehension about its potential impact on various professions, including accounting. The media often portrays a picture of AI-driven tools and systems replacing human accountants, stoking fears among small business owners that their trusted advisors may soon become obsolete. However, this argument overlooks the true potential of AI to augment, rather than replace, the skills and processes of accountants enabling them to provide even greater value to their small business clients. In this introduction, we will address the irrational fears, media hype, and fallacies surrounding the notion of AI replacing accountants.

Irrational Fears

Irrational Fears

The fear that AI will replace accountants is largely based on the misconception that AI can wholly replicate human skills, experience, and judgment. While AI-powered tools can automate routine tasks and improve accuracy, they cannot replace the nuanced understanding, empathy, and strategic thinking that human accountants bring to their work. In reality, AI serves as an invaluable tool that allows accountants to focus on higher-value tasks, providing tailored financial advice and fostering deeper relationships with their clients.

Media Hype

Sensationalist headlines and media reports often contribute to the misconception that AI is poised to replace accountants. However, this narrative tends to focus solely on the automation aspect of AI, ignoring the broader benefits of AI-augmented accounting. By understanding the true capabilities and limitations of AI, small business owners can better appreciate the complementary role that AI plays in enhancing the services provided by their accountants.

Fallacies in the Argument

The argument that AI will replace accountants is based on several fallacies:

AI can fully replicate human expertise:

While AI has made remarkable advancements, it is not capable of replicating the full range of human skills and expertise. Accountants possess years of education, experience, and professional judgement that AI systems cannot easily replicate.

Automation equals job loss:

Automation is often equated with job loss, but in the case of accounting, AI-driven automation allows accountants to focus on value-added tasks, improving their efficiency and quality of service.

AI will eliminate the need for human interaction:

Despite the increasing use of AI-driven tools, the importance of human interaction in the accounting profession remains paramount. Clients value the personal touch and trusted advice provided by their accountants, which cannot be replaced by AI.

The Advent of AI in Accounting

With a clear understanding of the irrational fears, media hype, and fallacies surrounding the notion of AI replacing accountants, we can now explore how AI is poised to augment the skills and processes of accountants enabling them to provide even greater value to their small business clients.

In the following sections, we will delve into the specific benefits AI-driven tools can bring to businesses with relevant and practical examples. We’ll look at how AI can enhance the capabilities of accountants including automating routine tasks, improving accuracy, enhancing fraud detection, streamlining tax compliance, and providing customised financial insights.

Automating Routine Tasks

One of the most significant ways AI can augment the skills of accountants is by automating repetitive and time-consuming tasks. Examples include data entry, transaction categorisation, and invoice processing. By automating these processes, accountants can spend more time focusing on providing strategic financial advice and analysis, ultimately offering small business clients a higher level of service and financial insight.

Practical example:

A small retail business generates numerous transactions daily, including sales, expenses, and payroll. An AI-powered accounting software can automatically categorise these transactions, eliminating the need for manual data entry. For instance, the software could identify a transaction from a supplier, match it with the corresponding purchase order, and update the accounts payable accordingly. This automation saves the accountant time and reduces the risk of data entry errors, allowing them to focus on more value-added tasks for their client.

Improving Accuracy and Reducing Errors

Human errors are inevitable, and accounting mistakes can be costly, especially for small businesses. AI algorithms can analyse large data sets with remarkable speed and accuracy, identifying discrepancies and potential errors. This increased precision helps accountants ensure their clients’ financial records are accurate, reducing the risk of costly mistakes and allowing small business owners to make well-informed decisions.

Practical example:

A small technology manufacturing company may struggle with inventory management, leading to errors in cost of goods sold calculations. An AI-driven accounting solution could analyse historical inventory data and automatically flag discrepancies, such as unusually high or low inventory levels. By identifying these potential errors early, the accountant can address the issue before it leads to inaccurate financial statements or tax filings.

Enhancing Fraud Detection and Prevention

Fraud and financial irregularities can severely impact small businesses. AI-driven accounting software can analyse vast amounts of data to detect unusual patterns, flagging potential fraudulent activities. By leveraging machine learning, these systems can continuously improve their detection capabilities, providing accountants with a powerful tool to protect their small business clients from financial fraud and potential legal issues.

Practical example:

A small creative consulting firm might be vulnerable to expense reimbursement fraud, where employees submit false or inflated expense claims. An AI-powered expense management system could analyse historical expense data and detect patterns that suggest fraudulent activity, such as unusually high expense claims from specific employees or locations. By alerting the accountant to these anomalies, the system can help prevent financial losses and protect the business’s reputation.

Streamlining Tax Compliance and Planning

Tax compliance is a critical aspect of accounting, and AI-powered tools can help accountants stay up to date with constantly changing tax regulations. By automating tax calculations and identifying potential deductions, AI allows accountants to optimise tax planning strategies for small business clients. This can result in significant cost savings, reduced risk of penalties, and more efficient tax preparation processes.

Practical example:

A small software development company needs to comply with various tax regulations, such as VAT and Corporation Tax. An AI-driven tax software could automatically calculate the company’s tax liabilities based on real-time financial data, ensuring that the accountant files accurate and timely tax returns. Additionally, the software could identify tax-saving opportunities, such as R&D tax credits, helping the business minimise its tax burden and optimise its financial planning.

Customised Financial Insights

AI-driven accounting software can provide accountants with in-depth financial analytics and forecasting capabilities. By analysing historical financial data and identifying trends, AI can help accountants offer tailored financial advice to small business clients. This personalised guidance can support better decision-making, enabling small businesses to optimise their financial performance and plan for future growth.

Practical example:

A small UK-based restaurant owner seeks advice on expanding their business. The accountant uses AI-powered financial forecasting software to analyse historical sales data, customer demographics, and seasonal trends. By identifying patterns and potential growth areas, the accountant can provide personalised advice on the optimal time and location for opening a new restaurant, helping the business owner make well-informed decisions based on data-driven insights.

Conclusion

Artificial intelligence is transforming the world of accounting, offering numerous benefits to both accountants and their small business clients. By automating routine tasks, improving accuracy, enhancing fraud detection, streamlining tax compliance, and providing customised financial insights, AI empowers accountants to deliver a higher level of service and value to small businesses.

As AI technology continues to advance, we can expect even more innovative solutions to emerge, further revolutionising the accounting industry and supporting small businesses’ growth and success. The practical examples provided, relevant to the UK market, illustrate the immense potential of AI-driven accounting solutions in enhancing the capabilities of accountants and delivering tangible benefits to small business clients.

Interpreting a balance sheet and how it can help you to make better business decisions

As a successful business owner, you understand that financial stability is key in order to maintain the longevity of your company; it’s essential for continued growth. One primary factor of achieving this goal is having an accurate understanding of one’s balance sheet and how each asset contributes to the overall picture. Furthermore, applying this to your clients and suppliers, can also provide valuable insights into the stability of your business overall!

Having resources available to decipher what affects or influences bottom-line numbers can assist you in making strategic decisions based on reliable data – so let’s dive into why understanding a balance sheet is important here!

Not all financial information is available all of the time

When assessing the viability of other companies, whether suppliers or clients, their annual accounts posted on Companies House may not provide a full set of financial reports, only the balance sheet may be available. As this is the most usual financial report available, we’ll look at the balance sheet in more detail below, but having access to income statements and cash flow statements would provide a more balanced view of a company’s financial standing. These may be possible to acquire if your company is entering into a more formal business relationship with the other party and as such would form part of your own due diligence process.

However, on its own, the balance sheet can still provide some useful first insights into a company’s standing, as well as your own.

Here are some of the questions we pose in this article:

- What is the balance sheet and why is it important to understand?

- What are the essential elements of a balance sheet that help somebody understand the health of a company?

- What are key ratios and how are these derived from a balance sheet?

- I’m looking at doing business with a new supplier, what specific aspects of their balance sheet should I be looking at?

- How can you use a balance sheet to assess whether a new client is worth doing business with?

What is the balance sheet and why it is important to understand?

A balance sheet is a financial statement that provides a snapshot of a company’s financial position at a given point in time. It summarises the company’s assets, liabilities, and equity, and is an important tool for assessing the financial health and stability of a company.

A balance sheet is particularly important for several reasons:

- Compliance: Companies are required by law to prepare and file annual financial statements, including a balance sheet, with Companies House. These statements must comply with the UK accounting standards, and failure to comply can result in penalties.

- Financial analysis: A balance sheet is a key tool for financial analysis, allowing investors, creditors, and other stakeholders to evaluate a company’s financial position and make informed decisions about whether to invest in or lend to the company.

- Decision-making: A balance sheet provides important information for decision-making within a company. For example, it can help management assess the company’s liquidity and working capital, which can inform decisions about capital expenditures, dividend payments, and other strategic initiatives.

- Transparency: A balance sheet provides transparency and accountability, allowing stakeholders to see how a company’s assets are deployed and how its liabilities are managed. This can be particularly important for companies with complex financial arrangements or significant debt.Understanding the elements of a balance sheet is an important part of smart financial management for any business owner. While it takes some training to intuitively understand how to interpret the information on balance sheets, keeping up with its evolution can be immensely beneficial for running a successful business. With an increasingly digital world, technology advancements have put critical data only a few clicks away, so it’s easier than ever to stay ahead of compliance regulations and use this data to make informed decisions about your finances. Whether you’re just getting started or are a seasoned veteran in the business ownership game, having awareness of the basics of a balance sheet can go a long way towards setting your company up for success.

What are the essential elements of a balance sheet that help somebody understand the health of a company?

There are three essential elements of a balance sheet that can help somebody understand the health of a company:

- Assets: Assets are what a company owns or controls, such as cash, inventory, property, plant and equipment, and investments. A strong balance sheet typically has a healthy mix of short-term and long-term assets, indicating that the company has enough resources to meet its obligations in the near term and invest in its future growth.

- Liabilities: Liabilities are what a company owes to others, such as loans, accounts payable, and deferred revenue. A strong balance sheet typically has a manageable level of liabilities relative to its assets, indicating that the company is able to meet its financial obligations.

- Equity: Equity represents the residual value of a company’s assets after its liabilities are subtracted. It includes items such as common stock, retained earnings, and other comprehensive income. A strong balance sheet typically has a healthy level of equity, indicating that the company has a strong financial foundation and is able to withstand economic shocks.

In addition to these essential elements, other factors that can help somebody understand the health of a company include the quality of the assets (such as whether they are depreciating quickly), the maturity and interest rate of the liabilities (such as whether they are due in the near term or the long term), and any off-balance sheet items that could impact the company’s financial health.

I’m looking at doing business with a new supplier, what specific aspects of their balance sheet should I be looking at?

As experienced accountants, we would recommend that you consider several specific aspects of a potential supplier’s balance sheet when evaluating their financial health. Also, if you can get hold of them, there are a few other factors you out to consider, we’ve included these too. Together these factors can provide valuable insights into the supplier’s liquidity, debt levels, inventory management, profitability, and ability to meet their financial obligations.

Liquidity:

When evaluating a supplier’s balance sheet, it is essential to consider their liquidity. This can be assessed by reviewing their current assets and liabilities. Current assets include cash, accounts receivable, and inventory, while current liabilities include accounts payable, short-term loans, and other short-term obligations. A supplier’s liquidity is crucial because it indicates their ability to pay their bills on time and keep their business running. If a supplier has a low current ratio, it could indicate that they may struggle to pay their bills on time or may be at risk of insolvency.

Debt levels:

The supplier’s debt levels are also an essential aspect to consider. Total debt includes short-term and long-term debt, such as bank loans, bonds, or other financing agreements. The debt-to-equity ratio is a crucial indicator that measures the amount of debt a company has compared to its equity. A high level of debt can be a warning sign of financial risk or potential difficulties in meeting their financial obligations. It is also essential to review their interest expense and maturity schedule of their debt to gain a better understanding of their ability to service their debt.

Accounts receivable:

The supplier’s accounts receivable balance and aging schedule are important to assess their ability to collect payments from customers. A high level of overdue accounts receivable may indicate potential cash flow problems or issues with their customer base. You want to ensure that the supplier has a low level of overdue accounts receivable and that they have efficient processes for collecting payments from their customers. Additionally, reviewing their credit policy and customer concentration can provide insights into potential risks in their accounts receivable.

Inventory turnover:

Assessing the supplier’s inventory turnover ratio is also important for understanding their inventory management practices. A low inventory turnover ratio may indicate potential obsolescence or inefficiencies in their operations, while a high inventory turnover ratio may indicate strong sales or efficient inventory management.

Gross margin:

The supplier’s gross margin can provide valuable insights into their pricing strategy and cost structure. A low gross margin may indicate pricing pressures or high costs that could impact their profitability, while a high gross margin may indicate strong pricing power or efficient cost management.

Working capital:

Reviewing the supplier’s working capital is important for assessing their ability to meet their short-term obligations. You should ensure that the supplier has sufficient working capital to cover their current liabilities, such as paying suppliers or employees. Additionally, reviewing their trade payable and receivable terms can provide insights into their cash conversion cycle and working capital management practices.

Capital expenditures:

Finally, reviewing the supplier’s capital expenditures is important for assessing their investments in property, plant, and equipment. You want to ensure that the supplier is investing in their operations and has the capacity to fulfill your business needs. Additionally, reviewing their depreciation schedule and asset quality can provide insights into their long-term capital investment strategy.

By considering these specific aspects of a potential supplier’s balance sheet, you can gain a deeper understanding of their financial health and make more informed decisions about whether or not to do business with them. As expert accountants, we are always here to provide guidance and support to help you make the best financial decisions for your business.

How you can use a balance sheet (and other reports if you can get them) to assess whether a new client or partner is worth doing business with?

Analysing financial health doesn’t have to be a daunting prospect. Evaluating key metrics like liquidity, debt levels, accounts receivable and inventory turnover can all provide insight into their ability to generate cash flow for the future. By taking time to understand these numbers as well as analysing potential clients’ capital expenditures are essential steps in determining whether they’re suitable for your business goals.

Review the current assets and liabilities:

By looking at a potential client’s current assets and liabilities, you can assess their liquidity and short-term financial health. Current assets include cash, accounts receivable, and inventory, while current liabilities include accounts payable, short-term loans, and other short-term obligations. You want to ensure that the client has enough current assets to cover their current liabilities. A high current ratio is generally seen as favourable, as it indicates that the client has sufficient liquidity to meet their short-term obligations.

Assess the long-term financial health:

To evaluate a potential client’s long-term financial health, you should review their total assets, liabilities, and equity. This will help you understand the client’s overall financial position and their ability to meet their long-term obligations. You should also review their debt-to-equity ratio to see how much debt the client is carrying compared to their equity. A high debt-to-equity ratio may indicate a high level of risk, as the client may have difficulty servicing their debt obligations in the long-term.

Analyse the accounts receivable:

The client’s accounts receivable can provide valuable insights into their credit and collection policies. You want to ensure that the client has an efficient process for collecting payments from their customers and that they have a low level of overdue accounts receivable. A high level of overdue accounts receivable may indicate potential cash flow problems or issues with their customer base.

Assess the profitability:

By reviewing the client’s income statement, you can assess their profitability and revenue trends over time. You should review their gross margin and net profit margin to understand how well the client is managing their costs and pricing their products or services. You can also review their revenue growth rate to see how their business is expanding over time.

Analyse the cash flow statement:

Analysing a potential client’s cash flow statement can help you understand how they generate and use cash, including cash flows from operating activities, investing activities, and financing activities. By reviewing their cash flow statement, you can assess their ability to generate cash and manage their cash flows effectively. A positive cash flow from operations is generally seen as favourable, as it indicates that the client has sufficient cash to fund their operations.

Review the working capital:

Reviewing the client’s working capital is important for assessing their ability to meet their short-term obligations. You should ensure that the client has sufficient working capital to cover their current liabilities, such as paying suppliers or employees. Additionally, reviewing their trade payable and receivable terms can provide insights into their cash conversion cycle and working capital management practices.

Assess the capital expenditures:

Finally, reviewing the client’s capital expenditures is important for assessing their investments in property, plant, and equipment. You want to ensure that the client is investing in their operations and has the capacity to fulfil their business needs. Additionally, reviewing their depreciation schedule and asset quality can provide insights into their long-term capital investment strategy.

By considering these specific aspects of a potential client’s balance sheet and other financial reports, you can gain a deeper understanding of their financial health and make more informed decisions about whether or not to do business with them. Additionally, being able to analyse the firm’s cash flow statement can provide valuable insights into their ability to generate and manage cash effectively, allowing you to make more informed business decisions.

Talk to TaxAgility about improving your business efficiency

TaxAgility are experts in analysing the performance of your company and helping you find ways to improve your business’s efficiency. If you’d like understand more about how we can help you manage your business, call TaxAgility today on 020 8108 0090.

Changes to the VAT Penalty System in 2023

Situations often arise where we are unable to hit payment deadlines, whether human error, or circumstances conspiring unfavourably, it happens. So, it’s good to see HMRC taking a positive stance in this regard, in its latest revision of the VAT penalty system. In this article, we’ll review the changes to the VAT system you can expect in 2023.

As of January 1 the default VAT penalty system has been replaced by a scheme that on the face of it seems to be less punitive for the occasional late payment or submission. The new system treats late submissions and payments separately. It also calculates interest on late payments differently too.

Period of familiarisation

While the new system is already in operation, HMRC has said that it will allow a period of ‘familiarisation’, to allow businesses to adjust. If your business misses a payment deadline, so long as the payment is made within 30 days, or if you have a ‘Time to Pay’ agreement in place, no penalty will be levied. This familiarisation period extends to December 31 2023.

How penalties are applied

The penalty system applies in two ways:

- Late VAT submissions

- Late payments

A new development is that late submissions for zero or even repayment returns can incur penalties under the new system.

One of the likely reasons for the new system is to help HMRC reduce the administrative overheads associated with chasing and processing late filings.

A new points system for late submissions

The new points system applies to VAT submission deadlines. It adopts a scheme similar to a driving licence. The more infractions a VAT payer racks up, the more points you get. Each time you miss a submission deadline, 1 point is added. The threshold at which a penalty is applied depends upon the filing submission period. These thresholds are given as:

- Annual – 2 points

- Quarterly – 4 points

- Monthly – 5 points

If you hit your threshold, you’ll incur a penalty of £200. If you continue to miss deadlines, you’ll continue to receive £200 penalties.

You won’t incur a penalty if:

- Your business is newly VAT registered and is your first VAT return

- You have cancelled your VAT registration and this is your business’s final VAT return.

- Single case VAT returns covering periods of a month, quarter or a year.

Can a business clear its accrued penalty points?

Driving licence points usually expire automatically after 4 years, not so with VAT penalty points.

For penalty points under the VAT system to expire, you will have to meet a test of good compliance. The period of time this applies for depends upon your submission period:

- Annual submissions: 24 months

- Quarterly submissions: 12 months

- Monthly submissions: 6 months

More information about the penalty points system can be found on the Government’s VAT site here.

Penalties for late payment

The new system aggressively targets late payers by introducing a two stage system that uses fixed penalties and then daily penalty charges. If your business has not paid its VAT bill and does not have a ‘Time to Pay’ agreement in place, it’s going to get expensive quickly.

Here’s a summary of how it works:

Up to 15 days overdue

The good news is the system does allow for circumstances where you may encounter some unavoidable delays in submission. So, if you have a problem, talk to HMRC as you won’t be charged a penalty if you pay the VAT you owe in full or agree to a payment plan on or between days 1 and 15.

Between 16 and 30 days overdue

If you are late in submission, your first penalty will be calculated at 2 per cent on the VAT you owe at day 15, IF you pay in full or agree a payment plan on or between days 16 and 30.

31 days or more overdue

For circumstances where your submission is 31 or more days late, then your first penalty will be calculated at a rate of 2 per cent on the VAT you owe at day 15 plus 2 percent on the VAT you owe at day 30.

As a further inducement to pay on time, HMRC will levy a second penalty which is calculated at a daily rate of 4 per cent for the duration of the outstanding VAT balance. This is calculated once the outstanding balance is paid in full or a payment plan is agreed.

Don’t forget about interest charges

Receiving a 2% penalty on late payments is only part of the overall costs you’ll incur. HMRC will continue to charge interest on late payments at a rate of 2.5% above the BOE base rate. This is even the case if you have an agreed ‘Time to Pay’ arrangement.

All is not equal under the sun where VAT repayments are concerned though. HMRC will only pay interest at a BOE rate -1% and a minimum rate of 0.5%! It’s probably best to ensure you get your payments correct.

Right to challenge

HMRC VAT right to challenge policy is a policy that allows taxpayers to appeal against HMRC tax decisions. This remains the same under the new scheme in 2023.

It is important for taxpayers to know their rights when it comes to challenging HMRC decisions, as this can help them ensure that they are not paying more than they should be.

Under the policy, taxpayers have the right to request a review of any HMRC decision within 30 days of receiving the decision letter. During this review process, HMRC will consider all relevant information and evidence provided by the taxpayer and make a new decision on the matter. This new decision may result in an increase or decrease in taxes owed, depending on the circumstances.

Taxpayers also have the option of appealing against HMRC decisions in certain cases. This involves submitting an appeal to an independent tribunal which will review all relevant evidence and decide whether or not HMRC’s original decision was correct.

Ultimately, understanding your rights when it comes to challenging HMRC decisions is essential for ensuring you are not paying more than you should be.

How HMRC can use its powers to enforce payment

- HM Revenue & Customs (HMRC) has a number of powers available to them which they can use to enforce payment and collect any amount outstanding. These include:

- Taking legal action, including issuing court summonses or seeking orders from magistrates’ courts.

- Making deductions from a person’s salary or pension payments.

- Placing a restriction on the bank accounts of individuals or businesses, preventing them from making any further transactions until their debt is paid off.

- Using third party debt collectors to chase up outstanding payments.

- Using bailiffs and seizing goods in order to cover the cost of unpaid VAT.

In extreme cases, HMRC may even take criminal action against someone who has deliberately evaded payment of their taxes, leading to potential fines and/or imprisonment. Therefore, it is important for businesses to ensure they remain compliant with all applicable legislation surrounding their VAT payments and make sure that all amounts due are paid on time in order to avoid any of these serious consequences.

Why it makes sense allowing a VAT professional manage your VAT submissions

VAT for all but the smallest VAT registered companies can be a complex affair where mistakes can easily be made. TaxAgility are experts in VAT and can remove the burdens of managing and calculating your VAT liabilities from your daily business management routine. We’ll ensure your VAT returns are accurate and make sure they are filed on time.

If you’d like to simplify your VAT management, call TaxAgility today on 020 8108 0090.

How to mitigate the impact of inflation on your business

Inflation is a major factor that entrepreneurs and small business owners must take into consideration when crafting their business plans and setting prices. With careful planning and adaptation, businesses of all sizes can weather the effects of rising prices and stay competitive in today’s economy. Inflation affects many areas of businesses, such as pricing strategies, supply chain costs and marketing. It is important to assess the effects of inflation on a regular basis in order to remain profitable and successful. With proper management and strategic decision-making, small business owners can successfully navigate through periods of rising prices. In this article, we take a look at how inflation affects businesses and what business owners and managers can do about it.

What is inflation and how does it impact businesses?

Inflation is an economic phenomenon that results in a general increase in prices over a period of time. It can have a significant impact on businesses as it affects the cost of production and the revenue generated. When inflation increases, businesses must pay more for materials, labour, and other costs associated with producing goods and services. This can lead to higher prices for consumers, reduced profit margins, and even layoffs if companies are unable to pass those additional costs onto their customers. Additionally, rising inflation levels may also cause people to reduce spending due to decreased purchasing power caused by higher prices. This can further reduce demand for products and services leading to further financial losses for businesses.

What are the different types of inflation?

Inflation is typically divided into three main categories:

- Demand-pull inflation

- Cost-push inflation, and;

- Built-in inflation.

Demand-pull inflation occurs when consumer demand for goods and services increases faster than the economy can produce them. This causes prices to rise as businesses try to keep up with consumer spending, leading to an overall increase in the general price level.

Cost-push inflation happens when the costs of production increase without a corresponding increase in consumer demand. Some examples include higher costs of labour, raw materials, or energy needed to produce goods and services. When these costs go up, businesses will often pass those added expenses onto customers by increasing their prices—which raises the general price level across the economy.

Built-in inflation is a type of inflation that tends to happen over time due to the natural expansion of an economy. This type of inflation is usually seen in developing countries, where economic growth has led to a surge in demand for goods and services, pushing up prices as the country’s ability to produce them struggles to keep up with demand.

Inflation can also be categorised based on its speed or rate at which it occurs. Hyperinflation is a type of rapid, out-of-control inflation that typically happens when too much money is printed without enough real resources or assets backing it. This leads to an increase in money supply, which causes prices for goods and services to skyrocket quickly. By contrast, mild or moderate inflation is a slower rate of inflation that does not cause dramatic fluctuations in the general price level.

Overall, different types of inflation can have a huge impact on an economy, so it’s important to understand each type and how they are related. By recognising the various causes of inflation, governments and businesses can be better prepared to respond appropriately and reduce its negative effects.

How can a business protect itself from the effects of inflation?

One way businesses can protect themselves from inflation is by budgeting for it in advance. By staying abreast of current financial trends, business owners can plan ahead for any increases in the cost of goods or services due to inflation. This requires an understanding of the current market conditions, so business owners should keep a close eye on economic indicators such as the Consumer Price Index (CPI).

Businesses can also adjust their pricing to account for inflation. This may mean increasing prices in order to remain profitable, or it could involve finding ways to cut costs without sacrificing quality or customer satisfaction. Business owners should also look into hedging techniques such as futures contracts, options trading, and other methods of protecting against currency fluctuations due to inflation.

Finally, businesses need to be aware that inflation can affect the value of their investments and should monitor their portfolios to ensure they are not exposed to excessive risks. By taking proactive steps to protect against inflation, businesses can remain financially secure despite economic uncertainty.

What are some strategies for reducing the impact of inflation on a business?

One strategy for reducing the impact of inflation on a business is to increase operational efficiency. This is an area TaxAgility can assist with. We can help businesses review their operating costs and identify areas where they can improve efficiency, reduce waste, and save money. Additionally, businesses should look for opportunities to diversify their operations or enter new markets that may be less sensitive to inflationary pressures.

Businesses should also consider hedging strategies when dealing with inflation. Hedging involves taking measures to limit losses due to price fluctuations in commodities or currency exchange rates by investing in derivatives or forward contracts. This allows businesses to protect themselves from spikes in prices due to inflation and ensure that their operations remain profitable even amid unpredictable economic conditions.

In addition, businesses should consider diversifying investments by investing in a variety of different asset classes such as stocks, bonds and commodities. Diversification helps protect businesses from the effects of market volatility and can help ensure the long-term financial stability of a business even amid periods of high inflation.

Finally, businesses should seek out financing sources that offer fixed rates of interest. This will allow them to protect their profits from the effects of inflation and reduce the overall cost of debt financing.

These are just a few strategies for reducing the impact of inflation on a business. Business owners and executives should work with their financial advisors to identify which tactics might be most beneficial for their particular operations. By taking proactive steps to manage inflation risk, businesses can protect themselves against unexpected changes in prices and ensure long-term profitability.

How can businesses stay ahead of the curve when it comes to inflation?

In short, planning, foresight and common sense. By taking a proactive approach to inflationary pressures, businesses can ensure that they are well-prepared for any possible changes in the economy. They should be prepared for various scenarios and have contingency plans in place to address them. This includes developing the strategies mentioned above for hedging currency fluctuations or investing in different asset classes that can provide some protection from inflationary pressures. Businesses should also consider ways to reduce their operational costs, such as utilising energy efficiency measures or outsourcing services that would otherwise be costly in house. Taking these steps can help businesses stay afloat during periods of economic volatility caused by inflation and remain competitive in the long run.

How TaxAgility can help your business fight inflation

At TaxAgility, we don’t just provide an accounting service, we’re an extension of your financial team. We are here to help you identify the ways best suited to your unique business to fight the impact of inflation. We can help you do this by ensuring you maintain proper up to date management accounting information which allows you day-by-day to track income and expenses and the impact of rising costs on profit margins and cash flow.

We’re here to assist and advise as problems and opportunities arise. Call us today to discuss how we can help you keep a lid on the inflation’s impact on your business. Call today on: 020 8108 0090.

Note: This article is not intended to provide financial advice or guidance, it is for interest only.

A Guide to Understanding and Improving Your Balance Sheet

Understanding and managing your business’s balance sheet is an essential part of any successful company. A balance sheet is a financial statement that provides a snapshot of what you own (assets) and what you owe (liabilities). It's important to keep track of this information so that you can stay within your budget, pay off debt, and make sure your cash flow is healthy. Let's take a look at how to understand and improve your balance sheet.

Understanding and managing your business’s balance sheet is an essential part of any successful company. A balance sheet is a financial statement that provides a snapshot of what you own (assets) and what you owe (liabilities). It's important to keep track of this information so that you can stay within your budget, pay off debt, and make sure your cash flow is healthy. Let's take a look at how to understand and improve your balance sheet.

Components of a balance sheet

A balance sheet is a financial document that provides an overview of the company’s assets, liabilities, and equity. It shows the business’s net worth and provides detailed information about the company’s assets (what it owns) and liabilities (what it owes).

A balance sheet is made up of three components: assets, liabilities, and equity. Assets are anything that has value for the company and can be used to generate income or pay expenses. Examples include cash, accounts receivable (money owed to the company from customers), inventory, buildings, equipment, investments, or trademarks. Liabilities are any debts or obligations that the company owes money on. These can include loans, mortgages, credit cards, accounts payable (money owed by the company), accrued expenses (like wages or taxes), or other debts that need to be paid off in the future. Equity is the difference between all the assets and liabilities, it's what's left over after all debts are paid off. This includes any profits that have been retained by the business rather than distributed as dividends to shareholders.

Tips for improving your balance sheet

Once you have an understanding of what makes up your balance sheet, you can start making improvements. Start by looking for ways to reduce expenses; for example, renegotiating contracts with suppliers or seeking out cheaper sources for materials or services. You can also look for ways to increase profit; for example, expanding into new markets or offering new products/services. Finally, review your debt level; if they are high then consider refinancing them through lower interest loans which could save you money in the long run.

- Monitor Cash Flow: Monitoring your cash flow will help you ensure that you have enough money on hand to cover expenses. This will also help you avoid overdrawing from accounts or taking out unnecessary loans.

- Utilise Loans Wisely: Use any loans you take out wisely by paying them back on time and using them for their intended purpose only. Taking out more than necessary in loans can increase interest payments over time, which can affect your bottom line negatively.

- Consider Investing: Investing in stocks, bonds, mutual funds, or other investments can help grow your business’s asset portfolio over time, meaning more money available for future projects or expansion opportunities down the road. However, be sure to do research before investing so that you know exactly where your money is going.

- Reevaluate Expenses: Take some time to regularly review expenses for any unnecessary items that could be cut back on or eliminated altogether in order to save money in the long run. This could include things such as subscriptions or memberships that may not be used often enough to justify their cost each month.

How to read your balance sheet

The best way to read a balance sheet is to start with understanding its structure. The left side of the balance sheet should contain all assets listed in order from most liquid (cash) to least liquid (tangible assets like buildings). The right side should contain all liabilities listed from most current (accounts payable) to least current (long-term debt). Once you understand how a balance sheet is organised you can begin reading it more thoroughly looking at each asset and liability individually. This will give you an idea of how much money is coming into your business versus how much money is going out, and if there’s enough left over for profit!

- Cash: Cash on hand plus any short-term investments in marketable securities

- Accounts Receivable: Money owed by customers for goods or services provided

- Inventory: Goods held for sale by the business

- Buildings: Long-term real estate investments owned by the company

- Equipment: Tools used for production or office use owned by the company

- Investments: Securities such as stocks and bonds owned by the company

- Trademarks: Intellectual property owned by the company

- Loans: Loans taken out by the business from banks or investors

- Mortgages: Long-term loans taken out from lenders secured against real estate investments

- Credit Cards: Credit card balances owed to creditors

- Accounts Payable: Money owed by businesses to vendors/suppliers

- Accrued Expenses: Expenses incurred but not yet paid such as wages/taxes

- Long Term Debt: Debt obligations due more than 12 months in future

- Equity: Difference between total assets & total liabilities; retained earnings plus capital stock issued minus dividends paid out

Being aware of what goes on with your business’s balance sheet is essential if you want to succeed in managing finances effectively and staying within budget constraints while still growing financially over time. By monitoring cash flow carefully, utilising loans wisely when needed, investing strategically when possible, reevaluating expenses regularly, businesses will be well equipped with the knowledge they need to maintain a healthy balance sheet year after year!

Also, your balance sheet is an essential component of your management reporting. It gives you clear insight into your business’s financial health, providing instant access to the essential financial data required to make smart management decisions. From recording cash payments and invoices to reconciling cloud accounting transactions, the balance sheet can help you benchmark performance and position yourself for future growth. With easy-to-read insights, however complex your management report may be, the balance sheet clearly displays key performance indicators that reveal the true picture of your finances.

Choose TaxAgility as your accounting services provider

With these tips in mind, understanding and improving your balance sheet should become easier, allowing your business to achieve success without compromising its financial health!

Naturally, with TaxAgility as your accounting services provider, we can help you improve the financial strength of your company and lessen the burden of managing balance sheets and management reporting through our cloud based accounting solutions. Just call us today on 020 8108 0092 and find out how.

2023 trends businesses can embrace in the search for competitiveness

Developing or adjusting your business plan for the coming year, will likely take into account many of the broader economic factors that may affect you, such as the economic outlook, inflation, interest rates, supply chain issues and money supply. However, businesses are also affected by trends, such as customer expectations, enabling or disruptive technologies, working patterns, and societal values. These are more intangible, but nevertheless can have a significant impact on a business’s success. In this article we will look at some of the prominent trends in 2023.

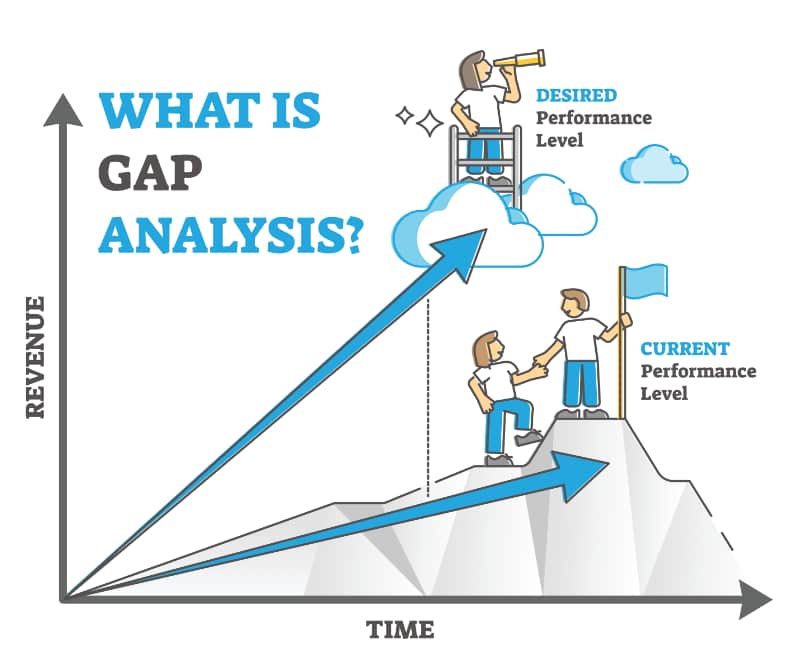

Identifying trends and revisiting the GAP Analysis

Trends are powerful market signals that shouldn’t be ignored. However, understanding exactly how they may apply to your business can be a little more difficult to interpret, as they may or may not have an impact on many areas of your product or service, or even how your business operates or is perceived from a brand perspective by your customers and market in general. This is where a little bit of analysis and a tool called GAP analysis comes in handy.

A GAP analysis is a simple tool that takes data and observations from your customers, market and competitors and makes sense of where others may be focused or not. It allows a business manager to spot where competition is especially strong and why, and therefore probably best to avoid. It also shows where competitors may be weak, perhaps from the perspective of a whole product or down to specific features. Weakness may be because of a lack of customer interest or market demand, but for the savvy business person, it might be because the area or niche may not have been explored or developed yet. This is where monitoring trends is especially powerful, as it may point to an opportunity to leverage a trend to develop an area of business others may have ignored because of market weakness.

A GAP analysis is a simple tool that takes data and observations from your customers, market and competitors and makes sense of where others may be focused or not. It allows a business manager to spot where competition is especially strong and why, and therefore probably best to avoid. It also shows where competitors may be weak, perhaps from the perspective of a whole product or down to specific features. Weakness may be because of a lack of customer interest or market demand, but for the savvy business person, it might be because the area or niche may not have been explored or developed yet. This is where monitoring trends is especially powerful, as it may point to an opportunity to leverage a trend to develop an area of business others may have ignored because of market weakness.

Performing a GAP analysis in concert with a regular review of your market and competitors, is a powerful way to spot opportunities that others may have missed. Smaller businesses simply can’t be everywhere at once and so tend to focus on specific areas of their market or certain features of a product that customers really like. As time goes by, trends will likely force small businesses to shift focus, sometimes subtly, other times though, quite significantly. As with the impact of Covid, some businesses had to fundamentally change the way they managed and engaged with the clients. This showed a lot of businesses new ways to be successful. However, many couldn’t meet the challenge and closed.

Where does the data to power a GAP Analysis come from?

There are different ways to conduct a gap analysis, one is to look at your business strategy and goals and where you’d like to be in the future, then identify the aspects of the business that you need to achieve your goal that currently are not in place. Another is to examine the strengths and weaknesses of a product and service compared to your competition and perceived market demand, or more importantly when considering trends - future market demand.

Essentially though, the analysis requires you to break down your product or service’s main features, pricing, distribution capabilities and other aspects of your business that contribute to market success. Then do the same for each of the main competition products. As you do this, rate them from 1 to 10 in terms of strength or attractiveness.

It requires some pretty extensive research, even maybe a little covertly as you try and peer into your competitor’s operation. Eventually though, you’ll start to see aspects of your product or service that either outperform, under perform or are completely missing from your’s or their offering. Add in the consideration for current and upcoming trends, and you’ll start to see areas where maybe you could outperform your competitor (or market), by acting early. You may even realise that your competitor is already doing this!

There are many sources of data for this research, examples are:

- Search engine searches around products, features, and capabilities will yield a fair amount of information.

- Independent market analysis reports that highlight company and product capabilities.

- Product comparison sites set products or services against each other and may also tear down products to examine how they are built.

- Annual reports, shareholder reports, investor analysis.

- Buy some of your competition’s products and test them yourself.

What are some of the trends small businesses will likely experience in the company year that businesses can explore and potentially plug into a GAP analysis?

Sustainability and brand responsibility

Consumers are becoming more sensitive to sustainability issues in their purchasing habits. While many are seeking to minimise the purchase of products that employ single use plastic, others are looking deep at the products themselves, for instance, once they have outlived their useful life, can they be reused for something else. Or, if they break, can they be repaired? Many products are simply not worth sending back to a manufacturer for repair, but just like used cars, some products can find repair solutions from third party providers.